The Landlord’s Guide to Cosigners

Some landlords agree to consider cosigners as long as they pass a background check, while other landlords don’t allow them at all. Since there are no laws that require you to accept a cosigner, according to RentPrep, it’s up to you to determine what makes the most sense for your property.

This guide will explain what a cosigner is, when someone might consider a cosigner when evaluating an applicant, the pros and the cons to having a cosigner on a lease and how to screen tenants and their cosigners.

What is a cosigner?

According to Nolo, a cosigner is a person designated to make the rental payments if the tenant does not pay. They sign their name to the lease agreement and are held fully responsible for rent if the tenant stops paying rent.

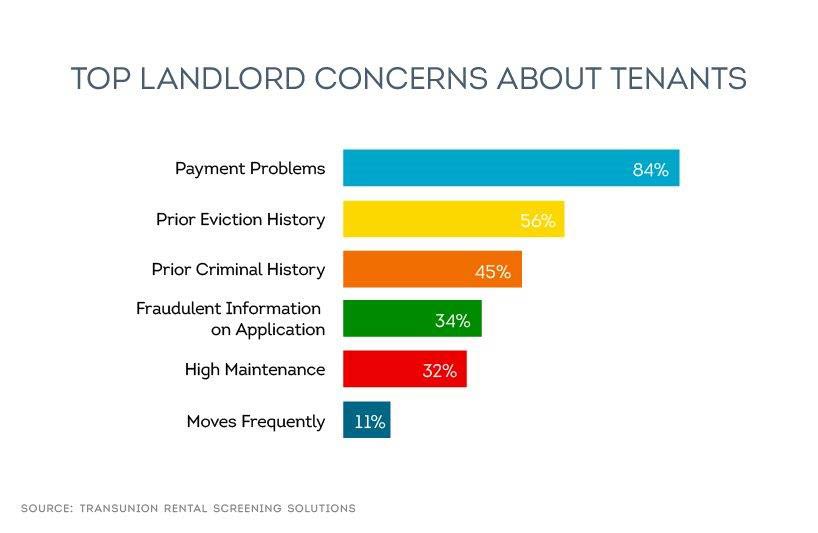

This can be a helpful assurance for landlords since TransUnion data shows that rent payment problems are a landlords’ number one concern with new tenants.

Apartment Guide points out that a cosigner gives you more options should something go wrong. Depending on your state laws, you may be able to pursue payment from both parties simultaneously or go straight to the cosigner. Since late payments can ding both the credit of the tenant and their cosigner, the cosigner has motivation to remedy the situation quickly.

Why some applicants use a cosigner

Some people might decide to get a cosigner because they have no significant credit history (such as college students), or don’t meet the income requirements. Perhaps they are self-employed and it is harder for lenders and landlords to accurately gauge their actual earnings.

In these types of cases, they may request a friend or relative to cosign. This way, they can qualify for an apartment they might not qualify for on their own. If a landlord chooses to report on-time rent payments to a credit bureau, these could have a positive impact on the tenant's credit history.

How a cosigner helps fill vacancies

RentPrep compares having a cosigner to having insurance, when you’re considering an applicant who might otherwise not meet your rental criteria. According to You Check Credit, an appropriate cosigner agreement should make the cosigner jointly responsible for all the financial obligations of the tenant, including the security deposit, rent, fees, and charges related to damages.

Accepting a cosigner can help you fill vacancies when the market is tight, while helping to ensure that you have recourse if the rent isn’t paid on time. Rather than simply denying an applicant with a bad credit score or low income, you can choose to accept them and help mitigate your risk with a cosigner.

The pros and cons of having a cosigner on a lease

PROS

A cosigner could help you protect your rental income while allowing you to be more flexible with your renting criteria. For instance, college students or younger renters may not have had enough time to build their credit history. There may be other circumstances, such as medical bills or unemployment that may make an otherwise good tenant appear risky on paper.

Some landlords would rather accept a higher deposit than add a cosigner to the lease. According to Zillow, however, there may be state or local housing laws that cap the amount you set. For example, you may not be able to charge more than two month’s rent as a security deposit. If the security deposit isn’t enough to recoup your losses in the case of non-payment or damages, having a cosigner may be the better option.

CONS

No Nonsense Landlord points out that a cosigner does not help with risk based on a tenant’s personal behavior, which is separate from financial risk. For example, having a cosigner isn’t going to help with problems such as noise complaints, unneighborly behavior, or utility shutoff. You’ll still want to screen your tenant carefully.

There may be some circumstances where having a cosigner may not be the answer. If a tenant doesn’t have a high enough income to cover rent, it’s likely that you’ll be chasing down rent from both parties and that means more work for you. If a person has a relevant criminal record, having a cosigner may not mitigate the risk involved.

When to consider running a background check on a cosigner

When it comes to conducting a tenant screening on all parties (especially if you have multiple tenants on the lease), you want to be sure you know who you are dealing with on all levels. That way, you have a more complete picture on both who will be living in your home and who will be responsible for rent.

You Check Credit reminds landlords that a cosigner is responsible for their own housing costs, as well as potentially those of the tenant’s. You need to be able to determine whether the cosigner has the resources to take on all of these financial obligations. Since you may have to deal with them as you would a tenant should the necessity arise, you’ll want to screen a cosigner as thoroughly as you did the applicant.

Conclusion

As an independent landlord, you have the ability to determine the best decision for your rental property. If you do decide to accept a cosigner, you should be sure to complete a thorough tenant screening on that person as well. This is one of the best ways to ensure that your investment is protected.

With TransUnion SmartMove, you can screen potential tenants and cosigners in a matter of minutes without having to store their personal information. SmartMove offers a renter credit report, rental criminal background check, and national eviction report, so you have a more complete picture of their background. With reliable information delivered from TransUnion, you can feel more confident in your decision to accept a tenant with a cosigner.

<< Back